The single fastest way to earn more airline miles isn't flying more. It's not using shopping portals or joining dining programs — though those help.

It's getting the right credit card.

A well-chosen travel credit card can generate 60,000–100,000+ bonus miles in your first few months, earn 2x–5x on categories you already spend in every day, and unlock transfer partners that turn ordinary bank points into Business Class flights on some of the world's best airlines.

A poorly chosen one earns 1 mile per dollar on everything, charges a $550 annual fee, and delivers almost nothing in return.

This guide cuts through the noise. We've broken down the best travel credit cards for earning points and miles in 2026 — by earn rate, transfer partners, annual fee, and most importantly, which type of traveler each one actually suits.

One important note before we dive in: sign-up bonuses, earn rates and annual fees change regularly. Always verify the current offer directly with the card issuer before applying. The details here reflect typical current market rates as of mid-2026.

What Makes a Great Travel Credit Card?

Before the card-by-card breakdown, here's what actually matters:

- The sign-up bonus: The single biggest miles event you'll encounter. Top cards offer 60,000–100,000+ bonus miles after meeting a minimum spend threshold in the first 3 months. That alone is often enough for a round-trip Business Class flight.

- Everyday earn rates: The multipliers you earn on every purchase — 1x, 2x, 3x, 4x. Higher earn on categories where you spend heavily (dining, groceries, travel) compounds significantly over time.

- Transfer partners: Some cards earn flexible points currencies — Chase Ultimate Rewards, Amex Membership Rewards, Capital One Miles, Citi ThankYou Points — that transfer to multiple airline programs. This flexibility is enormously valuable. Others earn directly into a single airline's program.

- Annual fee vs. value delivered: A $550 annual fee card can absolutely be worth it — if the credits, lounge access and earn rates exceed that cost for your lifestyle. A $95 card that doesn't match your spending habits can be a waste. Run the numbers honestly.

- Point value: Not all points are equal. 1 Chase Ultimate Rewards point is typically worth more than 1 basic cash-back point because of its transfer partner network. The card's earning currency matters as much as the earn rate.

Quick Comparison: The Best Travel Credit Cards for 2026

|

Card |

Points Currency |

Best Earn Rate |

Annual Fee |

Transfer Partners |

Best For |

|

Chase Sapphire Preferred |

Chase UR |

3x dining, 2x travel |

$95 |

United, Southwest, BA, Air France, Singapore Airlines, Aeroplan + more |

Beginners, everyday earners |

|

Chase Sapphire Reserve |

Chase UR |

3x dining, 3x travel, 10x hotels via Chase |

$550 |

Same as Preferred |

Frequent travelers, lounge users |

|

Amex Gold |

Amex MR |

4x dining, 4x US supermarkets, 3x flights |

$250 |

Delta, BA, Singapore Airlines, ANA, Air France + more |

Foodies, grocery shoppers |

|

Amex Platinum |

Amex MR |

5x flights (direct/Amex Travel), 5x hotels (Amex Travel) |

$695 |

Same as Gold |

Luxury travelers, lounge regulars |

|

Capital One Venture X |

Capital One Miles |

2x everything, 5x hotels/car rental, 10x via C1 Travel |

$395 |

Air Canada, Turkish, Singapore Airlines, Air France, Avianca + more |

Simplicity seekers, premium earners |

|

Citi Strata Premier |

Citi ThankYou |

3x air, hotels, dining, supermarkets, gas |

$95 |

Turkish Miles&Smiles, Avianca, Singapore Airlines, Air France + more |

Value seekers, diverse spenders |

|

Chase Freedom Unlimited |

Chase UR* |

1.5x everything, 3x dining/drugstores |

$0 |

Unlocked via Sapphire card |

Companion card for Chase ecosystem |

|

United Explorer Card |

United MileagePlus |

2x United, restaurants, hotels |

$95 |

United MileagePlus direct |

United loyalists |

|

Delta SkyMiles Gold Amex |

Delta SkyMiles |

2x Delta, restaurants, US supermarkets |

$150 |

Delta SkyMiles direct |

Delta loyalists |

|

American Airlines Platinum Select |

AAdvantage |

2x American, restaurants, gas |

$99 |

AAdvantage direct |

American Airlines loyalists |

*Chase Freedom Unlimited earns points that can only be transferred to airline partners when combined with a Chase Sapphire card in the same household.

The Best Flexible Points Cards (The Most Powerful Earners)

These cards earn points in a flexible currency — not tied to a single airline — giving you the freedom to transfer to whichever program offers the best redemption for your specific trip.

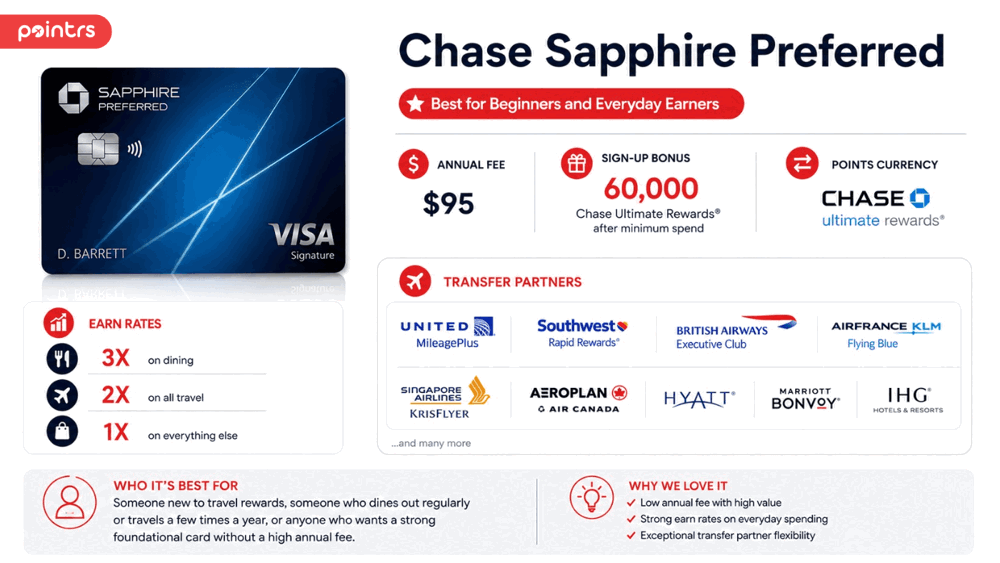

Chase Sapphire Preferred — Best for Beginners and Everyday Earners

Annual fee: $95

Earn rates: 3x on dining, 2x on all travel, 1x on everything else

Sign-up bonus: Typically 60,000 Chase Ultimate Rewards points after minimum spend

The Chase Sapphire Preferred is the card most points experts recommend as a first travel card — and for good reason. The $95 annual fee is low, the earn rates are strong on the two categories most people spend heavily on (dining and travel), and the transfer partner list is exceptional.

Transfer partners include: United MileagePlus, Southwest Rapid Rewards, British Airways Avios, Air France/KLM Flying Blue, Singapore Airlines KrisFlyer, Air Canada Aeroplan, Hyatt, Marriott, IHG, and others.

That flexibility means your points aren't locked into one airline. Book United domestically. Transfer to Singapore Airlines for a Southeast Asia trip in Business Class. Use Avios for short-haul American Airlines flights. One card, multiple strategies.

Who it's best for: Someone new to travel rewards, someone who dines out regularly or travels a few times a year, or anyone who wants a strong foundational card without a high annual fee.

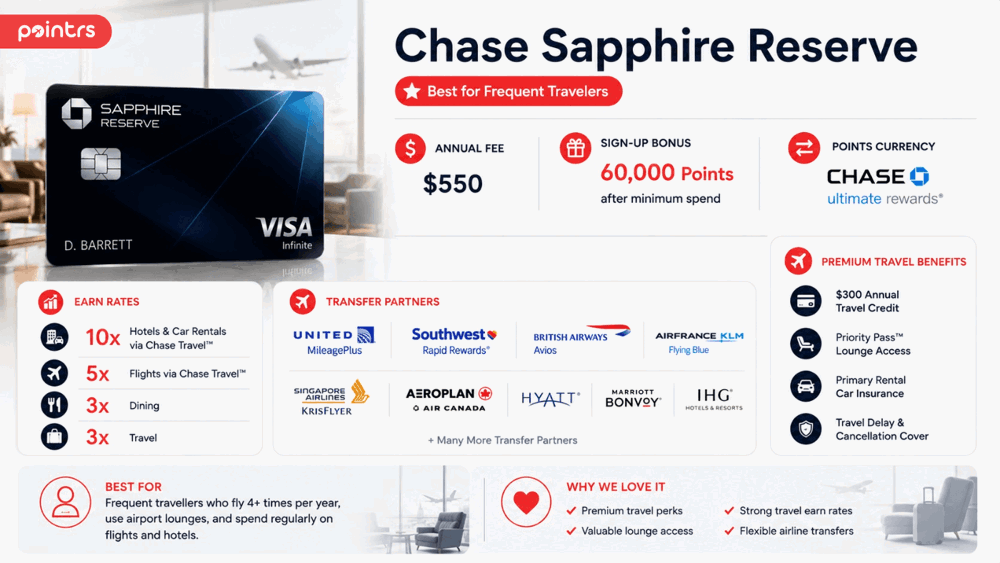

Chase Sapphire Reserve — Best for Frequent Travelers

Annual fee: $550

Earn rates: 3x on dining and travel, 5x on flights through Chase Travel, 10x on hotels and car rentals through Chase Travel

Sign-up bonus: Typically 60,000 Chase Ultimate Rewards points after minimum spend

The premium version of the Preferred. Same transfer partners, higher earn rates on travel, and a suite of travel benefits that offset much of the annual fee — including a $300 annual travel credit (applied automatically to travel purchases), Priority Pass airport lounge membership, primary rental car insurance, and travel delay/cancellation coverage.

The math on the annual fee: The $300 travel credit alone brings the effective cost down to $250. Add lounge access, travel insurance, and higher earn rates on travel spend, and for a frequent traveler the Reserve quickly pays for itself.

Who it's best for: Someone who travels 4+ times a year, uses airport lounges, and already spends significant money on flights and hotels. If you're only traveling once or twice a year, the Preferred is the better starting point.

American Express Gold Card — Best for Dining and Grocery Spend

Annual fee: $250

Earn rates: 4x at US supermarkets (up to $25,000/year, then 1x), 4x at restaurants worldwide, 3x on flights booked directly or through Amex Travel, 1x on everything else

Sign-up bonus: Typically 60,000–100,000 Amex Membership Rewards points after minimum spend. Sign up for a bonus here.

The Amex Gold's headline numbers are hard to argue with. 4x at US supermarkets and 4x at restaurants are among the best multipliers available anywhere — and these are categories where most American households spend thousands of dollars per year.

A household spending $600/month at supermarkets and $400/month at restaurants earns 48,000 Membership Rewards points per month from those two categories alone. That's 576,000 points per year. From groceries and dining.

Transfer partners include: Delta SkyMiles, Air Canada Aeroplan, British Airways Avios, Singapore Airlines KrisFlyer, ANA Mileage Club, Air France/KLM Flying Blue, Emirates Skywards, Avianca LifeMiles, and others.

The $250 annual fee is offset partially by a $120 dining credit (at Grubhub, The Cheesecake Factory, Goldbelly, Wine.com, and other partners) and a $120 Uber Cash credit, bringing the effective cost to around $10/year for those who use both.

Who it's best for: Anyone who cooks at home (Woolworths), eats out regularly, or wants premium earn rates without the Platinum's $695 price tag. One of the best-value earn cards in the market.

American Express Platinum Card — Best for Luxury Travelers

Annual fee: $695

Earn rates: 5x on flights booked directly with airlines or through Amex Travel, 5x on prepaid hotels booked through Amex Travel, 1x on everything else

Sign-up bonus: Typically 80,000–150,000 Amex Membership Rewards points after minimum spend

The Platinum isn't an everyday earn card — its 1x on most purchases means you'd pair it with the Gold or another card for daily spending. What it offers instead is an unmatched travel experience and a benefits package designed to offset its annual fee for heavy travelers.

Benefits that chip away at the $695 fee:

-

$200 annual airline fee credit

-

$200 hotel credit (prepaid bookings via Fine Hotels + Resorts or The Hotel Collection)

-

$200 Uber Cash ($15/month, $35 in December)

-

$240 digital entertainment credit ($20/month across select services)

-

$155 Walmart+ credit

-

Access to Amex Centurion Lounges, Priority Pass, Delta Sky Clubs (when flying Delta), and more

Add it up and the credits alone can exceed the annual fee for a traveler who uses them. The Platinum is less a points-earning machine and more a premium travel membership — with miles as a significant bonus.

Who it's best for: Frequent international travelers who value lounge access, luxury hotel upgrades, and premium travel protections. Those who book flights directly and want 5x earn on that spend specifically. Not the right first card.

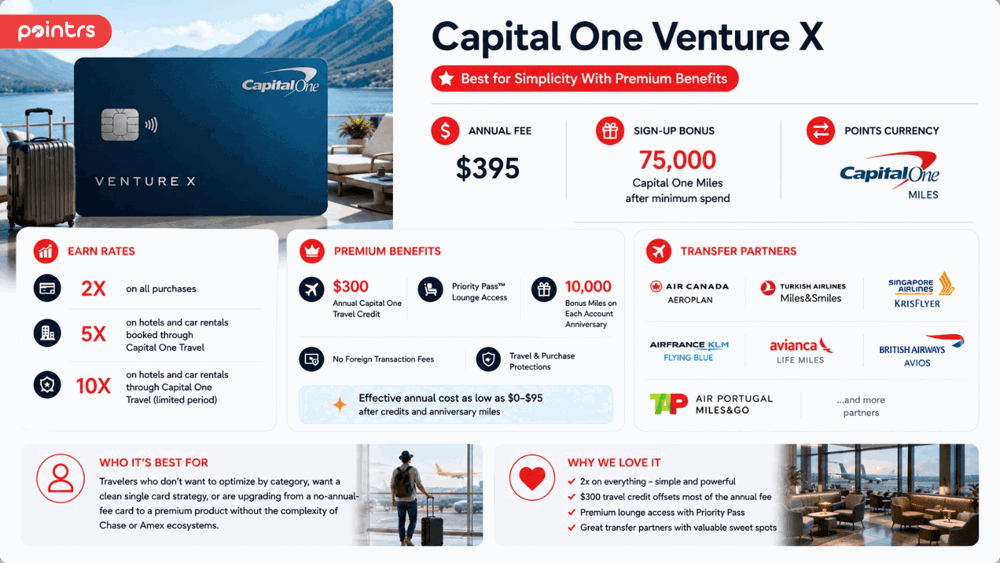

Capital One Venture X — Best for Simplicity With Premium Benefits

Annual fee: $395

Earn rates: 2x on all purchases, 5x on hotels and car rentals booked through Capital One Travel, 10x on hotels and car rentals through Capital One Travel (limited period)

Sign-up bonus: Typically 75,000 Capital One Miles after minimum spend

The Venture X is the most straightforward premium travel card on the market. 2x on everything means you never have to think about categories. Pair that with a $300 Capital One Travel credit, Priority Pass lounge access, 10,000 bonus miles on each account anniversary, and you have a card whose effective annual cost after credits and anniversary miles is closer to $0–$95 — despite the $395 listed fee.

Transfer partners include: Air Canada Aeroplan, Turkish Airlines Miles&Smiles, Singapore Airlines KrisFlyer, Air France/KLM Flying Blue, Avianca LifeMiles, British Airways Avios, TAP Air Portugal Miles&Go, and others.

Turkish Airlines Miles&Smiles is a sleeper standout in this list — it allows redemptions on Star Alliance partners (including United and Lufthansa) at extremely competitive rates, sometimes far lower than booking directly through United MileagePlus.

Who it's best for: Travelers who don't want to optimise by category, want a clean single card strategy, or are migrating from a no-annual-fee card to a premium product without the complexity of Chase or Amex ecosystems.

Citi Strata Premier — Best Value Mid-Tier Card

Annual fee: $95

Earn rates: 3x on air travel, hotels, restaurants, supermarkets, and gas stations, 1x on everything else

Sign-up bonus: Typically 70,000 Citi ThankYou Points after minimum spend

The most underrated card in the US travel credit card market. At $95, the Citi Strata Premier earns 3x across five high-spend categories — dining, groceries, gas, hotels, and air travel. No other card at this price point comes close to that category breadth.

Transfer partners include: Turkish Airlines Miles&Smiles, Avianca LifeMiles, Air France/KLM Flying Blue, Singapore Airlines KrisFlyer, Cathay Pacific Asia Miles, Virgin Atlantic Flying Club, and others. No domestic US airline direct transfers — but Turkish Miles&Smiles gives you United redemptions, and Air France Flying Blue covers Delta and other SkyTeam carriers.

Who it's best for: The points player who wants strong everyday earn across multiple categories without a high annual fee. A compelling standalone card, and an excellent companion to Chase or Amex primary cards.

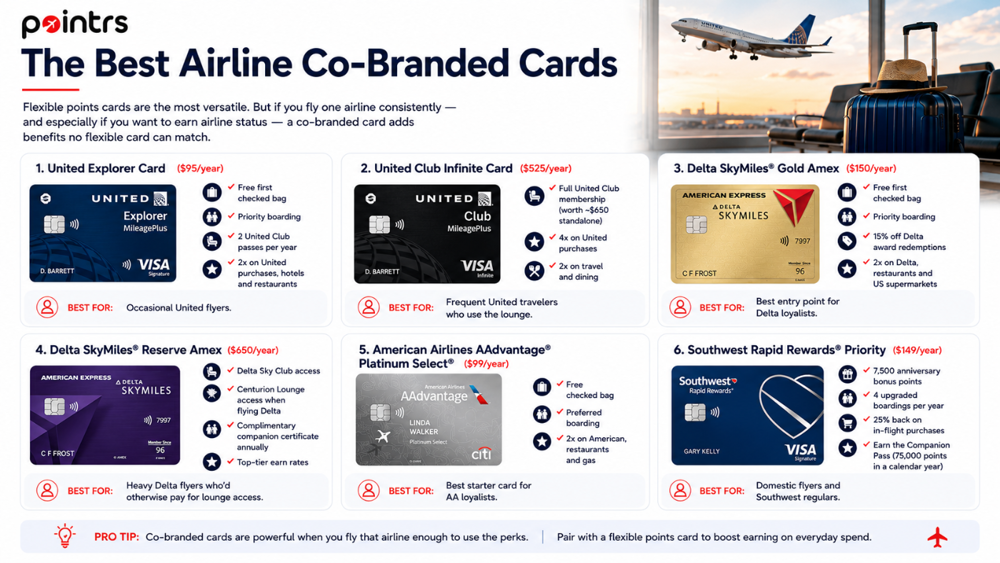

The Best Airline Co-Branded Cards

Flexible points cards are the most versatile. But if you fly one airline consistently — and especially if you want to earn airline status — a co-branded card adds benefits no flexible card can match.

- United Explorer Card ($95/year): Free first checked bag, priority boarding, 2 United Club passes per year, 2x on United purchases, hotels and restaurants. Best for occasional United flyers.

- United Club Infinite Card ($525/year): Full United Club membership (worth ~$650 standalone), 4x on United purchases, 2x on travel and dining. Best for frequent United travelers who use the lounge.

- Delta SkyMiles Gold Amex ($150/year): Free first checked bag, priority boarding, 15% off Delta award redemptions, 2x on Delta, restaurants and US supermarkets. Best entry point for Delta loyalists.

- Delta SkyMiles Reserve Amex ($650/year): Delta Sky Club access, Centurion Lounge access when flying Delta, complimentary companion certificate annually, top-tier earn rates. Best for heavy Delta flyers who'd otherwise pay for lounge access.

- American Airlines AAdvantage Platinum Select ($99/year): Free checked bag, preferred boarding, 2x on American, restaurants and gas. Best starter card for AA loyalists.

- Southwest Rapid Rewards Priority ($149/year): 7,500 anniversary bonus points, 4 upgraded boardings per year, 25% back on in-flight purchases, and the key to earning the coveted Companion Pass (75,000 Rapid Rewards points in a calendar year). Best for domestic flyers and Southwest regulars.

How to Choose the Right Card for You

If you're just starting out: → Chase Sapphire Preferred. Low annual fee, strong earn rates, excellent transfer partners, and a sign-up bonus that can fund your first award flight. The ideal foundation card.

If you spend heavily on dining and groceries: → Amex Gold. 4x on both categories is best-in-class. Pair it with a no-annual-fee Amex card (like the Blue Business Cash) for everyday purchases.

If you travel frequently and want lounge access: → Chase Sapphire Reserve or Amex Platinum. Both deliver lounge access and substantial travel credits. The Reserve is better for general travelers; the Platinum is better for luxury-focused, flight-heavy spenders.

If you want simplicity: → Capital One Venture X. Flat 2x on everything, premium benefits, manageable effective annual fee. One card, no category management.

If you fly one airline almost exclusively: → That airline's co-branded card, layered on top of a flexible points card. Get the bag fee waivers, boarding benefits and status credit boosts from the co-branded card; earn your base points on the flexible card.

If you want maximum value on a budget: → Citi Strata Premier + Chase Freedom Unlimited (no annual fee). Combined earn across dining, groceries, gas, travel, and general spending — total annual fee under $100.

Can You Have More Than One Travel Card?

Yes — and most serious points earners do.

The most common and effective setup is a two-card combination:

-

A high-earn category card (like Amex Gold for dining and groceries)

-

A catch-all card for everything else (like Capital One Venture X at 2x, or Chase Freedom Unlimited at 1.5x)

Some experienced players run a three-card stack:

-

Chase Sapphire Reserve (dining and travel earn + transfer access)

-

Amex Gold (supermarkets and international dining)

-

Chase Freedom Unlimited (1.5x on everything else, no annual fee)

The key discipline: make sure the combined annual fees are justified by the value you extract, and that you're feeding points into one primary program rather than splitting across too many.

Frequently Asked Questions

What's the best travel credit card for beginners?

The Chase Sapphire Preferred is the most consistently recommended starting point. The $95 annual fee is low, the sign-up bonus is strong, and the Chase Ultimate Rewards transfer partner network gives beginners flexibility to learn the system without being locked into one airline.

Is the Amex Platinum worth the $695 annual fee?

For the right traveler — yes. If you use the $200 airline credit, $200 hotel credit, $200 Uber Cash, lounge access and other credits, the effective annual cost can drop to near zero. If you won't use those benefits regularly, the Amex Gold is a better value.

What's the difference between transferable points and airline miles?

Airline miles (like Delta SkyMiles or United MileagePlus miles) are locked to one program. Transferable points (like Chase Ultimate Rewards or Amex Membership Rewards) can be moved to multiple airline and hotel programs, giving you flexibility to find the best redemption for your specific trip. Transferable points are generally more valuable for that reason.

How much is a sign-up bonus actually worth?

It depends on the points currency and how you redeem. A 60,000 Chase Ultimate Rewards sign-up bonus is worth a minimum of $750 in cash-back value — but transferred to United, Singapore Airlines or Air France, it can unlock a Business Class flight worth $3,000–$5,000+. Sign-up bonuses are consistently the fastest way to earn a meaningful redemption quickly.

Can I get multiple sign-up bonuses?

Yes, though each card issuer has its own rules. Chase has an informal "5/24 rule" — they typically won't approve new applicants who have opened 5 or more cards across any issuer in the past 24 months. Amex limits each person to one welcome offer per card "per lifetime." Capital One and Citi have their own restrictions. Understanding these rules matters if you're planning to apply for multiple cards over time.

Should I get a card that earns miles directly or one that earns flexible points?

Start with flexible points unless you have a very strong loyalty to one specific airline and fly it almost exclusively. Flexible points give you room to learn, experiment and find the best redemptions across programs before committing.

Already Have One of These Cards? Find Out What You Can Book Right Now.

Knowing your card earns points is one thing. Knowing exactly what flight you can book with your current balance — today, on a route you actually want to fly — is something else entirely.

That's Pointrs.

Add your points and miles balance and see every Earn More and Spend Less opportunity mapped out for you — in real time. No spreadsheets. No guesswork. No staring at an airline website wondering if your balance is enough.

Information in this article is accurate as of mid-2026. Credit card terms, annual fees, earn rates, sign-up bonuses and transfer partner arrangements are subject to change at any time. This article is for informational purposes only and does not constitute financial advice. Always verify current offers directly with card issuers before applying.